Welcome to "The Silverback Letter" by Mining Stock Monkey

Why the gold and silver Royalty Majors will grow faster than the Juniors

The Silverback Letter by Mining Stock Monkey

Issue #1

February 18, 2026

In the world of primates, the dominant Silverback is the undisputed troop leader. His primary role is protection. His focus is survival.

This mirrors my approach to the markets.

A Silverback is typically quiet and calm. He is patient. He conserves energy while the rest of the troop screeches at the noise. But when he acts, he does so decisively and aggressively.

Many investors obsess over the potential for a 100% or 1,000% gain. I obsess over the risk of a 75% loss.

Why?

Because the math of recovery is brutal: lose 75%, and you need a 300% gain just to get back to square one.

Defense first.

If I can manage my downside risk, the winners will take care of themselves.

My “default” setting is protection. Like a Silverback guarding the troop, I am risk-averse and slow to move. I don’t chase every new shiny object. But when a true asymmetric opportunity reveals itself, I flip the switch.

In the world of mining stocks, you survive by being conservative and you win by betting big when the odds are heavily in your favor.

I resonate with what Jim Rogers said in his Market Wizards interview. To roughly quote him:

The key to investing is simple. You just sit there doing nothing until you see a pile of money sitting in the corner and then you go and pick it up.

What is The Silverback Letter?

My specific portfolio allocations, dynamic valuation models, and specific buy and sell targets are reserved exclusively for Mining Stock Monkey premium subscribers.

The Silverback Letter is where I share the thesis behind the moves.

This letter is dedicated to my high-level view of the market: how I’m separating the signal from the noise, my take on sector news, and where I am currently seeing pockets of value and risk.

Think of this as the strategic map. The premium service provides the specific coordinates.

Why the major royalty companies will grow faster than the juniors

In issue #1 of The Silverback Letter, I’d like to share my thoughts on why the major precious metals royalty and streaming companies will enjoy more growth in the coming years than their smaller peers.

The majors are often criticized by investors who say they’re too large to experience meaningful growth — that if you want significant growth, you have to go with the smaller companies.

This is often true in terms of assets they already own, however, I see three major problems with this thinking:

The majors own a lot of royalties and streams on exploration and development assets, so they have growth built in.

The juniors are already valued by the market based on certain development projects coming into production. Therefore, the advanced development assets that they own are mostly priced into the stocks.

This ignores how fast the companies will grow from reinvesting their future cash flow. In this area, the juniors start off with a major disadvantage.

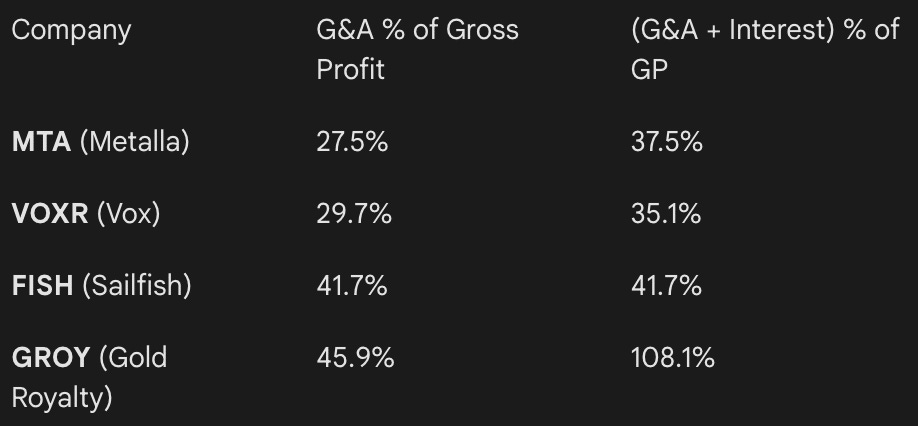

Q4 numbers will be released in the coming days but the charts below shows what percentage of gross profit was spent on G&A and servicing their debt in Q3 2025.

Junior Royalty Companies:

In this chart we can see that the junior royalty companies are typically using about 40% of their gross profit just to service their debt and cover “general and administrative” expenses.

This means that only about 60% of their gross profit is left to pay income tax and buy new assets to maintain or grow the business.

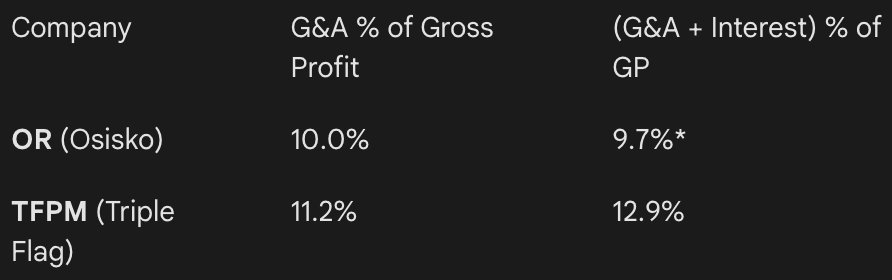

As we move up into the mid tiers, the numbers get much better.

Mid-tier Royalty Companies:

The mid tier companies OR Royalties (formerly Osisko) and Triple Flag Precious Metals spend about 10-13% of their gross profit on G&A and interest. This leaves them with ~90% of their gross profit to pay income tax and buy additional assets.

Note: The * indicates that OR had interest revenue that exceeded their interest expense, which helped to offset their G&A expenses.

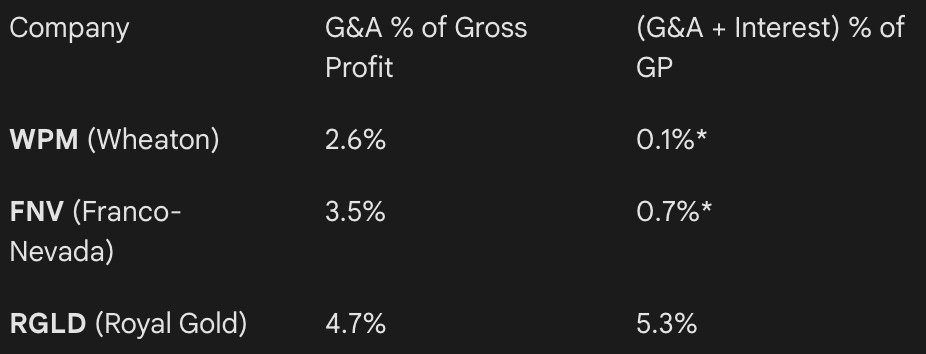

Finally, as we get into the majors, the numbers get even better.

Major Royalty Companies:

Because their businesses are so efficient, the super majors (WPM and FNV) have nearly 100% of their gross profit left over to pay tax and reinvest in their business, while the smaller major, Royal Gold, is left with 95%.

To illustrate the importance of reinvesting a higher percentage of gross profit...

Let’s say we have a company that reinvests 85% of gross profit after G&A, interest, and taxes. This represents “the major”.

And another that reinvests 60% after G&A, interest, and taxes. This represents “the junior”.

Both companies start out with $1,000,000

Both companies earn a 15% return on all investments

After 10 years, the company with the lower G&A is ~45% more valuable.

After 20 years, the company with the lower G&A is worth almost double.

After 30 years, the company with the lower G&A is worth almost triple.

After 40 years, the company with the lower G&A is worth quadruple.

In this example, the only difference between the two companies is that one company was more efficient with their corporate overhead than the other one.

Okay, but don’t the majors have to do huge transactions to realize meaningful growth?

Yes, the majors do need to deploy a significant amount of capital to see meaningful growth and the good thing is there’s no shortage of potential quality investments.

In the past year, Franco Nevada has invested $1.675 Billion into new large streams and royalties:

$250M for a royalty with I-80 gold

$100M into Orezone

$275M for a 1% royalty on Anglogold Ashanti’s “Arthur” project

$1,050M for a royalty from a third party on IAMGold’s Cote mine

In the past 12 months, Royal Gold has invested nearly $4.9 billion into major purchases:

$1 billion for a large gold stream on First Quantum’s “Kansanshi” copper mine

$196M to buy Horizon copper in an all cash transaction

$3.5 billion for Sandstorm Gold

$200M for a royalty and stream with Solaris Copper

And in the past 12 months, Wheaton Precious Metals has committed to major investments of ~$5.4 billion:

$4.3 billion for a large silver stream on Antamina (from BHP)

$330M for a gold stream on Hemlo

$670M for a gold stream on Spring Valley

$94M for a stream on Rio2’s Fenix Gold Project

The lists above ignore the companies’ minor purchases, but these three royalty majors are also making smaller investments into earlier-stage projects to help augment their long-term growth and secure the rights to finance promising early-stage projects.

The large investments won’t stop here

The world is going to need a lot of copper in the coming years and I believe precious metals streams will be an important funding mechanism for the companies who are putting large copper projects into projection.

These copper producers are going to need billions of dollars to build these mines and by selling a stream on byproduct gold and silver they improve two of their most important financial metrics — It allows them to increase their IRR and lower their payback period.

When the copper producer only enjoys a 7X multiplier on their copper cash flow while the precious metals royalty majors are rewarded with a 25X multiplier, both parties are incentivized to do these transactions.

There are only three royalty companies that have access to the amounts of capital needed to make these large deals happen: Wheaton Precious Metals, Franco Nevada, and Royal Gold.

Many people say that most of the growth of the major royalty companies is behind them — I think they’re only just getting started.

If you’re already a paid subscriber on miningstockmonkey.com, please don’t sign up for a paid substack subscription — it’s the same service on a different platform. We can upgrade your substack access upon request if you email us at hi@miningstockmonkey.com.